Can People With Disabilities Afford This Tax Cut?

By Annie Acosta, Director of Fiscal and Family Support Policy

May 1, 2017 – Washington, D.C. President Donald Trump released an outline of his tax reform proposal on April 26. In what he calls “the biggest individual and business tax cut in American History,” the President offers a plan than would disproportionately benefit the wealthiest of citizens and substantially add to federal deficits and the debt. Low income Americans, including the disproportionate number with disabilities, would eventually be faced with even greater cuts to critical federal programs to make up for the resulting budget shortfall.

President Trump’s 2017 Tax Reform for Economic Growth and American Jobs

“The Biggest Individual and Business Tax Cut in American History”

Goals for Tax Reform

- Grow the economy and create millions of jobs

- Simplify our burdensome tax code

- Provide tax relief to American families—especially middle-income families

- Lower the business tax rate from one of the highest in the world to one of the lowest

Individual Reform

- Tax relief for American families, especially middle-income families:

- Reducing the 7 tax brackets to 3 tax brackets for 10%, 25% and 35%

- Doubling the standard deduction

- Providing tax relief for families with child and dependent care expenses

- Simplification:

- Eliminate targeted tax breaks that mainly benefit the wealthiest taxpayers.

- Protect the home ownership and charitable gift tax deductions.

- Repeal the Alternative Minimum Tax.

- Repeal the death tax.

- Repeal the 3.8% Obamacare tax that hits small businesses and investment income.

Business Reform

- 15% business tax rate

- Territorial tax system to level the playing field for American companies

- One-time tax on trillions of dollars held overseas

- Eliminate tax breaks for special interests

Process:

Throughout the month of May, the Trump administration will hold listening sessions with stakeholders to receive their input and will continue working with the House and Senate to develop the details of a plan that provides massive tax relief, creates jobs, and makes America more competitive – and can pass both chambers.

To understand the impact of this tax plan on people with intellectual and developmental disabilities (I/DD) and their families, it is also necessary to look at some of the basic facts about current tax policy. As the leading charitable organization advocating on behalf of people with intellectual and developmental disabilities, The Arc seeks to ensure that federal funding for programs that help our constituents to live meaningful lives in the community is preserved.

Essential federal programs like Medicaid, Social Security, Supplemental Security Income, and the many discretionary programs – like education, housing, and employment – are all funded through tax dollars, whether through individual, corporate, payroll, excise, estate, or other taxes. As stated by former Supreme Court Justice Oliver Wendell Holmes, Jr., “taxes are the price we pay for a civilized society.”

In addressing the impact of the plan, it is necessary to look at the assumptions in the plan’s goals, along with some of the details of the proposed changes:

- Grow the economy and create millions of jobs is a basic goal and assumption of this plan. However, the argument that tax cuts will be made up for by increased economic activity has long been discredited by leading economists. At most, a small percentage can be recouped. Read more on this from the Committee for a Responsible Federal Budget.

- Simplify our burdensome tax code. Reducing the current 7 tax brackets to 3 tax brackets (for 10%, 25% and 35%) does little to make taxes any easier to complete. It would simply lower the amount of revenue generated.

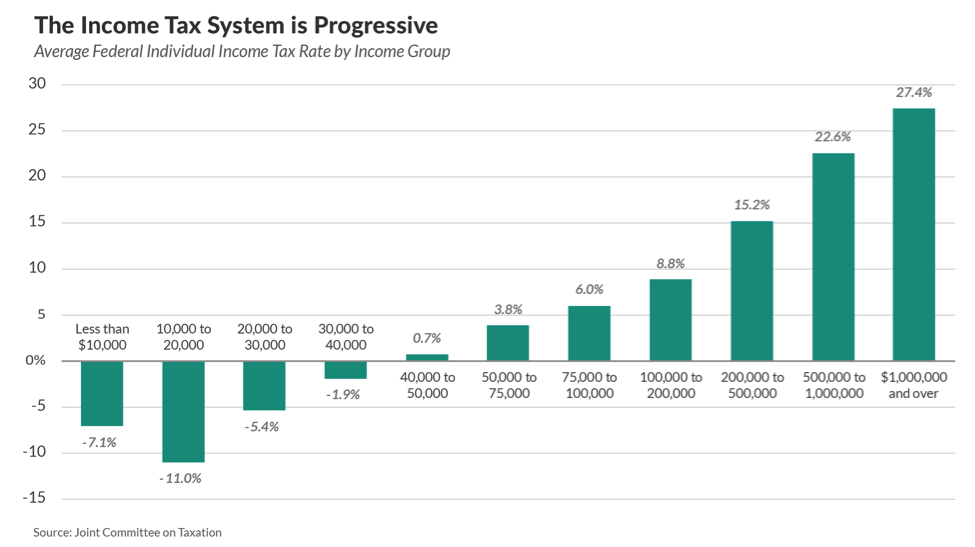

- Provide tax relief to American families, especially middle-income families. The implication that America is a high tax country is only true if the United States is compared to all nations, including the majority that are developing. When compared to other developed nations, the U.S. tax burden is below average. Learn more on comparative income taxes from the Pew Charitable Trusts.On average, Americans pay an effective income tax rate of 9.5 percent, according to research by the Tax Policy Center. As shown below, however, the federal tax system is progressive with middle income Americans paying a much lower rate. Those with incomes between $30,000 and $50,000 pay almost no federal taxes, and consequently, would stand to gain very little with the Trump tax cut plan.

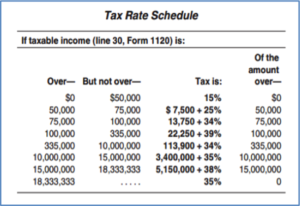

- Lower the business tax rate from one of the highest in the world to one of the lowest. While the top statutory corporate tax rate of 35% in the U.S. (shown right) is, in fact, among the highest, the effective tax rate is much lower. The average effective tax rate – the actual rate paid after deductions and credits – is slightly lower than other developed countries (27.1% versus 27.7%). See Congressional Research Service (CRS) report for more information.

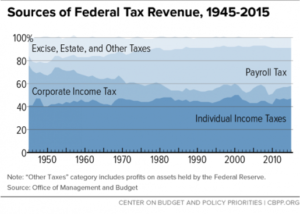

Further, it is important to note that corporate tax contributions have been steadily declining for decades. As shown below, the corporate share of federal tax revenue now only accounts for 11% of federal revenue, down by two-thirds in 60 years.

One of the reasons for this drop is changes in how corporations are operating and being taxed. An increasing number of corporations’ profits are subject to no taxation (foreign profits that stay abroad) or different taxes (income tax in the case of S corporations). S corporations are structured as “pass through” entities. They do not pay the corporate income tax, but rather pass profits through to owners who pay tax under the individual income tax at a lower rate. Over 90% of U.S. businesses do not pay the corporate tax rate.

One of the reasons for this drop is changes in how corporations are operating and being taxed. An increasing number of corporations’ profits are subject to no taxation (foreign profits that stay abroad) or different taxes (income tax in the case of S corporations). S corporations are structured as “pass through” entities. They do not pay the corporate income tax, but rather pass profits through to owners who pay tax under the individual income tax at a lower rate. Over 90% of U.S. businesses do not pay the corporate tax rate.

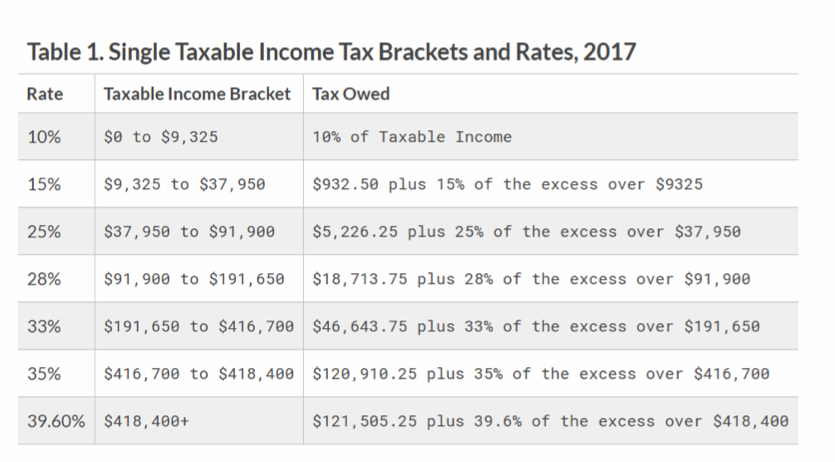

President Trump’s plan to allow S corporations to pay the proposed top business rate of 15% instead of the rate they pay under their current individual tax rate (see brackets below) would disproportionately benefit the very wealthy while draining public revenues. Currently, only individual income below $37,950 a year is taxed at 15 percent or less. Under the Trump plan, anyone who makes their income via a pass-through entity would pay the 15% rate no matter how much they made. President Trump owns over 500 such business entities, according to the Trump Organization’s tax counsel.

Source: Tax Foundation

Not explained in the President’s plan is that it will increase deficits by an additional $3 to 7 trillion over 10 years, according to the nonpartisan Committee for a Responsible Federal Budget . The proposed 60% cut in the corporate tax rate alone would lose $2.4 trillion over 10 years. Such massive cuts to revenues could have substantial impact on all human services funding, including services and supports for people with I/DD.

House and Senate leadership have consistently required that legislation be “paid for” in order to move through the legislative process and the President’s plan does not include viable pay-fors, therefore creating a major conflict if there is any interest in moving it forward. The Arc will remain vigilant in monitoring the impact of the plan if it begins to move legislatively.

For additional resources on federal taxes and the President’s plan see:

- https://www.crfb.org/blogs/fiscal-factcheck-how-much-will-trumps-tax-plan-cost

- https://www.cbpp.org/research/policy-basics-where-do-federal-tax-revenues-come-from

- https://www.forbes.com/sites/timworstall/2014/12/23/more-than-90-of-us-businesses-dont-pay-the-corporate-income-tax/#3bc328f35e48

- https://www.politifact.com/virginia/statements/2015/oct/20/donald-trump/trump-says-us-has-highest-tax-rate-anywhere-world/